During a recent internship in the OTC derivatives department of a securities firm, I worked on a project involving delta dynamic hedging for pricing vanilla options. Referencing John Hull's Options, Futures, and Other Derivatives, which covers delta hedging, I used Python to replicate the book's examples.

To hedge the risk of a sold call option, one must buy a certain number of shares. The number of shares purchased equals the call option's delta multiplied by the number of options sold. In this example, delta is 0.522.

The following sections show two hedging scanarios, corresponding to whether the option expires in the money or out of the money.

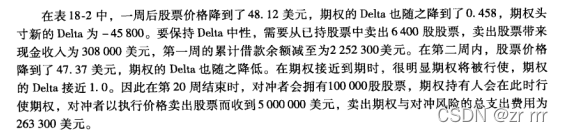

Scenario 1: The stock price at expiration is above the strike price, allowing exercise. The replication cost of the option is $263,300.

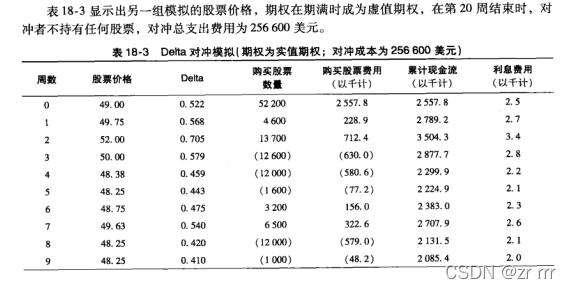

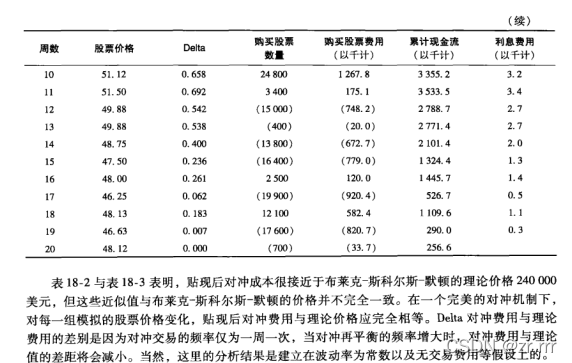

Scenario 2: The stock price at expiration is below the strike price, so the option expires worthless. The replication cost is $256,600.

Python Implementation

First, define a module bsm.py that calculates the value and delta of a call option under the Black-Scholes-Merton model.

from math import log, sqrt, exp

from scipy import stats

import numpy as np

class BSMOptionValuation:

def __init__(self, S0, K, T, r, sigma, div=0.0):

self.S0 = float(S0)

self.K = float(K)

self.T = float(T)

self.r = float(r)

self.sigma = float(sigma)

self.div_yield = float(div)

self.d1 = ((log(self.S0 / self.K) + (self.r - self.div_yield + 0.5 * self.sigma ** 2) * self.T) / (self.sigma * sqrt(self.T)))

self.d2 = self.d1 - self.sigma * sqrt(self.T)

def call_value(self):

return (self.S0 * exp(-self.div_yield * self.T) * stats.norm.cdf(self.d1, 0.0, 1.0) - self.K * exp(-self.r * self.T) * stats.norm.cdf(self.d2, 0.0, 1.0))

def delta(self):

delta_call = exp(-self.div_yield * self.T) * stats.norm.cdf(self.d1, 0.0, 1.0)

delta_put = -exp(-self.div_yield * self.T) * stats.norm.cdf(-self.d1, 0.0, 1.0)

return delta_call, delta_put

Then, replicate the case study. The following code uses the first stock price path (results match the book). You can test with the second path for verification.

from math import log, sqrt, exp

import numpy as np

import scipy.stats as si

from scipy.stats import norm

from bsm import BSMOptionValuation

import pandas as pd

if __name__ == '__main__':

# Option parameters

N = 100000 # Number of options

S1 = [49, 48.12, 47.37, 50.25, 51.75, 53.12, 53, 51.87, 51.38, 53, 49.88, 48.5, 49.88, 50.37, 52.13, 51.88, 52.87, 54.87, 54.62, 55.87, 57.25] # Stock price path 1

S2 = [49, 49.75, 52, 50, 48.38, 48.25, 48.75, 49.63, 48.25, 48.25, 51.12, 51.5, 49.88, 49.88, 48.75, 47.5, 48, 46.25, 48.13, 46.63, 48.12] # Stock price path 2

K = 50 # Strike price

r = 0.05 # Risk-free rate

sigma = 0.2 # Volatility

T = 0.3846 # Time to maturity (years)

simulation = 20 # Number of steps in the path

dt = T / simulation # Time step size

# Initialize structures

expire_time = np.append((np.ones((simulation, 1)) * dt).cumsum()[::-1], 0) # Remaining time to expiration

cash = np.zeros(simulation + 1) # Cash account

div = np.zeros(simulation) # Interest earned on cash

delta = np.zeros(simulation) # Delta values

# Hedging loop

for step in range(simulation + 1):

if step == 0: # Initial position

delta[step] = BSMOptionValuation(S1[step], K, expire_time[step], r, sigma).delta()[0]

cash[step] = delta[step] * N * S1[0] # Cash required to buy delta shares

div[step] = cash[step] * r * dt

elif step < simulation: # Rebalancing steps

delta[step] = BSMOptionValuation(S1[step], K, expire_time[step], r, sigma).delta()[0]

cash[step] = cash[step-1] + div[step-1] + (delta[step] - delta[step-1]) * S1[step] * N

div[step] = cash[step] * r * dt

else: # Settlement at expiration

if S1[step] > K:

cash[step] = cash[step-1] + div[step-1] - N * K

else:

cash[step] = cash[step-1] + div[step-1] - delta[step-1] * S2[step] * N

print(cash[-1]) # Option replication cost

Output for scenario 1:

263061.29677824676

This result closely matches the book's value of $263,300. The small discrepancy arises because the book rounds intermediate calculations to one decimal place. The result for the second stock price path is:

256520.06138881645

This is very close to the book's $256,600.

Next Steps

In practice, industry often uses cash delta rather than standard delta for dynamic hedging. Additionally, stock price paths can be simulated via Monte Carlo methods. The next article will demonstrate how to implement cash delta dynamic hedging using Monte Carlo simulation in Python.